26 executives from 18 companies participated in an event aimed at demystifying finance for non-finance people and highlighting the influence that managers from different areas of the business can have on the overall financial performance of their companies. Participants left with a better view of what finance is all about and important insights on how to successfully partner with their own company’s finance department.

The financial side of business decision making

Finance is really quite straightforward: Once you understand the language, the rationale behind seemingly complex terms becomes clear. For example, a credit default swap, or CDS, is merely an insurance for an underlying loan.

Despite growing liquidity resulting from rock bottom – and in some countries even negative – interest rates aimed at fostering economic growth, companies are finding it increasingly hard to manage financial pressures in terms of both raising capital and finding worthwhile opportunities to invest.

In this controversial environment, big international companies have been stockpiling their cash holdings for three main reasons: to ensure they have emergency funds to continue operations in an unstable geopolitical environment and turbulent commodity markets; to maximize tax efficiencies; and to make sure they have cash available to keep up with competition in terms of mergers and acquisitions. According to an article in The New York Times Magazine,1 in January 2016 American companies were holding around $1.9 trillion in cash (including short-term investments), of which Apple held over $200 billion, Microsoft held over $100 billion and Alphabet, Google’s new parent company, held around $80 billion.

These growing financial constraints combined with rising shareholder activism are making it even more complex to manage companies. Every business decision relating to strategy, operations, marketing, sourcing or any other area has financial consequences and will impact the firm’s profit and loss statement and balance sheet. For example, managers looking to increase business efficiency must consider all the knock-on effects that any actions will have on the company’s financial statements. For example, take a toy manufacturer, which operates in a highly competitive and seasonal industry. Its busiest period is the second half of the year due to peak events such as the start of the new school year, Thanksgiving and Christmas. From an operational perspective, seasonal business is inefficient because during the first semester, production is almost at a standstill whereas in the second semester it usually runs at full capacity. Spreading production evenly across the year may substantially improve operational efficiency, but since most sales occur during the second half of the year, the company’s inventory as well as the debt required to finance the additional production during the first semester will increase, and that translates into higher risk, thus making it even more difficult to raise financing.

Difficulties in Raising Capital

Despite expansionary monetary policies in most countries as well as steadily growing corporate cash holdings, many big brands are finding it hard to attract investors and raise capital. They need to consider not only where they can reach more active potential investors but also where their company has high potential to expand its revenues. For instance, Prada, an Italian fashion company, listed its shares on the Hong Kong Stock Exchange, purportedly to be closer to its growing, high-potential Asian markets. In June 2011 it raised $1.91 billion by listing 20% of its shares in Hong Kong, valuing the company at about $10 billion, i.e. 23 times its 2011 earnings. In contrast, in September 2014, a large Chinese e-commerce company launched an IPO on the New York Stock Exchange and raised a record $25 billion for the 14.9% of shares, valuing the company at around 22 times its 2013 earnings.

The finance side of value creation and value capturing

In the business world, value creation and value capturing reflect management effectiveness. Yet measuring these is quite challenging. Generally speaking, value created is the difference between the perceived value of a good or service minus the cost of producing (delivering) it, whereas captured value is the difference between the price at which a product or service is sold and the costs associated with producing and delivering it. Measuring perceived value – i.e. value created but not captured by the company – is complicated, but value captured can easily be measured in finance. Thus, when considering any major business decision, be it a potential investment or a new business model, it is useful to work out the financial calculations (i.e. pro forma financial statements) for each alternative to make it easier to understand and compare the long- and short-term revenues, costs and risks associated with each option.

To determine whether a company will be able to create value from an investment, two important things need to be calculated and considered: the cost of capital and the income it will generate. When a company borrows capital, it is has to pay a fee (e.g. interest). The total fee is referred to as the weighted average cost of capital (WACC). The income that is generated as a result of investing capital is called return on invested capital (ROIC). The WACC should obviously be lower than the ROIC. The economic value added (EVA) of capital is the difference between the return it generates and its cost, all multiplied by the amount of the invested capital (IC), i.e. EVA = (ROIC – WACC) * IC.

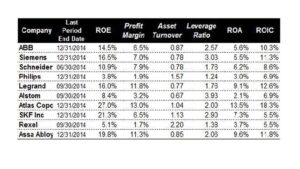

Another ratio commonly used to measure return on capital is return on equity (ROE). This is a very noisy performance indicator that combines three ratios: profit margin, which measures business efficiency or value created; asset turnover, which measures the efficiency of asset utilization or potential; and leverage ratio, which measures a company’s debt burden (see Figure 1). Raising capital in the form of debt has two major advantages: first, it has a lower required rate of return than equity (for the lender, debt is considered less risky than equity because in case of bankruptcy, debt owners will recuperate their investment before equity owners); second, interest on debt is tax deductible. So when a company reports an increase in ROE, it does not necessarily signify an improvement in business or asset efficiency. It could just be the result of pumped up debt, which is referred to as leverage. This was the case before the 2008 financial crisis when companies were reporting continuous growth of ROE but achieving this through intensive borrowing at cheap rates and in a loosely regulated environment.

Figure 1 : Return on equity formula

Return on assets (ROA) is another important performance indicator in capitalintensive industries like agriculture and manufacturing, where asset utilization and efficiency are vital for keeping up with competition and quite hard to improve.

ROE and ROA differ across industries and do not present a complete picture of return on capital. Return on invested capital (ROIC) is the ratio of operating income (as opposed to net income), which includes interest payments on debt minus taxes over the invested capital (sum of debt and equity minus cash holdings). ROIC shows how efficiently a company has used all the capital it has invested, regardless of whether that capital is equity and/or debt. It is an important ratio used in capital budgeting, intra-division capital allocation, performance measurement and as a key performance indicator (KPI) to calculate compensation. It paints a much more accurate picture than the more commonly used ROE, which can easily be manipulated by increasing the leverage. When making investment decisions, the ROIC should also be compared to the cost of capital to determine how much value is created by the capital employed.

In general, to obtain a complete picture of a company’s performance and efficiency, all three indicators (ROIC, ROE and ROA) should be considered both historically and in comparison with competitors and industry benchmarks (see Figure 2).

Figure 2 : Comparing indicators to measure a company’s performance

Obviously, increasing a company’s business and operational efficiency is one of the drivers of improved financial performance. Private equity firms are excellent at chasing business efficiency as they make money in two ways: through leverage buy-out (LBO), which means acquiring a company by raising debt, and through advantages in operations (i.e. improving business efficiency). However, many private equity firms tend to focus on short- and medium-term improvements and profits. CEOs and company owners are more focused on the long-term survival and performance of the organization, which necessarily takes into account the political, social and economic background, leaving little freedom to increase shortand medium-term efficiency.

Some executives mistakenly believe that in a context of intensifying competition and eroding margins, the only way to increase value created and captured is to grow internally and through acquisitions. But if internal growth is not supported by sizable returns (i.e. where the ROIC is significantly higher than the WACC), solvency will become increasingly problematic as returns no longer suffice to cover the growing leverage. This was what happened at Royal Bank of Scotland, which grew rapidly through acquisitions to become the fifth-largest bank in the world in terms of market cap and the secondlargest in the UK and Europe. It then nearly collapsed in 2008 because of its over-reliance on short-term wholesale funding and its high risk appetite among other things. It only survived as a result of being partly nationalized.

Growth through mergers and acquisitions (i.e. external growth) does not guarantee value creation either, because most organizations that pursue such a strategy fail to succeed in creating value. The only ones that do manage to do so are those that make post-merger integration a priority before making the deal and that focus on executing the integration swiftly.

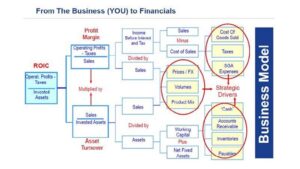

From you to financials

Finance is just a set of tools that are often misused and misunderstood, and blamed when the company fails. To better understand the financial consequences of everyday business decisions, managers should understand how their decisions affect the company’s financials.

Figure 3 illustrates how a company’s business model and its strategic drivers can affect its profit margin and ultimately its ROIC. For instance, decisions made by Procurement will affect the cost of goods sold, inventories, accounts payable, etc.; Marketing’s decisions on prices, product mix and production volumes will affect sales, general and administrative (SGA) expenses, etc. Besides being aware of the financial implications of their decisions, managers should also focus on increasing the efficiency of the resources under their control.

Figure 3 : From the business (YOU) to Financials

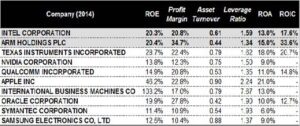

Figure 4 shows how different business models for the same final product lead to distinct financial outcomes. ARM and Intel produce the same end product – computer chips – but the way they do so differs substantially. Intel develops and manufactures them whereas ARM only does research and development and then licenses the intellectual property rights to the whole ecosystem of companies that produce chips, including Apple, Samsung and Qualcomm. For the end consumers of the products, the result is the same. But the financials of these two companies differ substantially: ARM’s profit margin and return on capital is much higher and thus more attractive and exciting for investors.

Figure 4 : Different Business models for the same end product

Conclusions

Finance is straightforward once you grasp the language and logic behind it. It provides analytical tools that can help managers make better-informed decisions, all of which will somehow affect financial performance. Higher risks should bring higher returns, but growth does not necessarily result in value creation. Value is only captured when investments generate higher returns than the cost of capital (be it debt or equity) required to finance them. It is thus important for managers to explore the consequences of various options, because what may appear to be a logical solution to improve efficiency, could in fact turn out to be more costly when all parameters are taken into account.

Discovery Events are exclusively available to members of IMD’s Corporate Learning Network. To find out more, go to www.imd.org/cln

Founded in 1994, Portfolio Advisors is an experienced private markets manager with dedicated primary, secondary, co-investment, real estate and direct credit teams. In 2023, Portfolio Advisors combined with FS Investments, a pioneer in the democra...

AI is revolutionizing finance, boosting productivity and insights, but CFOs must invest in infrastructure, navigate regulations, and upskill teams for a successful future.

Explore top books, websites, and podcasts recommended by IMD expert Jim Pulcrano for anyone venturing into or exploring venture capital, from entrepreneurs to investors.

As CIO at VenCap, David Clark leads the Investment Team, developing the firms’ investment strategy, fund identification, selection and monitoring. Founded in 1987, Vencap is one of the longest-established investment management and advisory firms a...

Anne has recently been named the CFO of a large multinational manufacturing group. It is a big change of direction: before this, she worked as a senior consultant with a top consultancy. Her appointment stems from a long and successful relationshi...

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications

Research Information & Knowledge Hub for additional information on IMD publications